Chart shows how many investors could be better off under CGT changes

- 3 minutes ago

- 2 min read

Housing has formed a major part of the 2026 federal budget, and property, along with other assets, are set be taxed differently. But what are the likely impacts?

What has been announced

From 1 July 2027, the 50% capital gains tax (CGT) discount that applies to assets held for more than one year will revert to an indexation method that was in place until 1999.

In general, those changes mean that realised capital gains will be taxed only on the asset's real return.

So, when someone sells an asset, be it a property or otherwise, after holding for at least one year, the purchase price is adjusted to sale-year prices using the consumer price index. The sale price less the inflated purchase price is the amount of taxable capital gains.

That is then taxed at either an income earner’s marginal rate or 30% - whichever is larger at the point of sale.

Newly built residential properties will be exempt. The change includes pre-1985 assets which were previously exempt.

Could the new inflation method benefit investors?

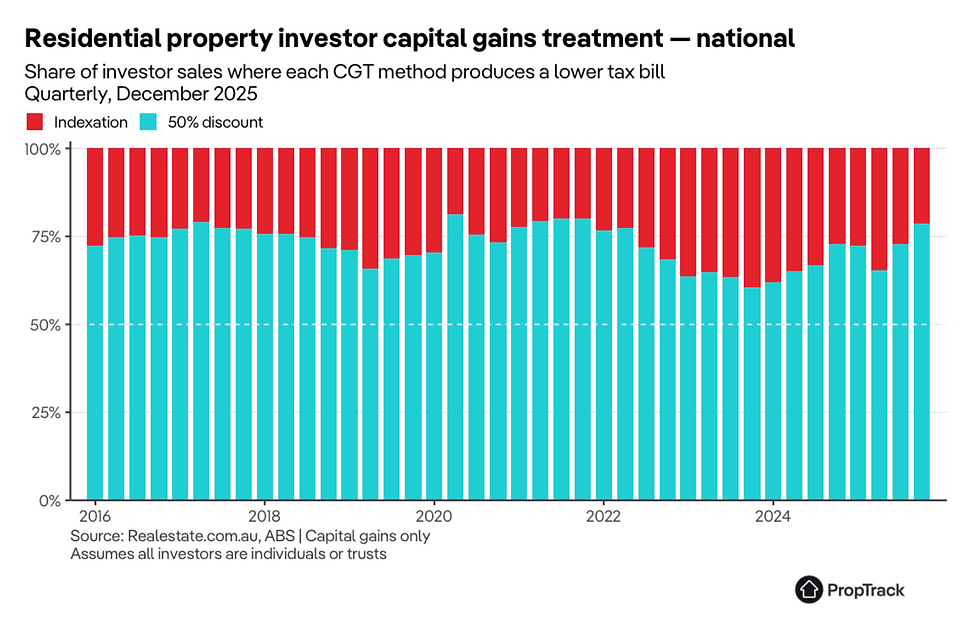

Analysis by realestate.com.au comparing the capital gains tax outcomes under the blanket 50% discount vs. the new inflation model shows that, for some residential property investors, the new tax treatment would have been more beneficial - meaning, it results in a lower taxable gain than an investor would have achieved under the 50% discount.

The new tax treatment favours investors during periods of lower capital growth. Over the past decade approximately 27% of properties that received a capital gain would have been better off under the new indexation model rather than the 50% discount.

This peaked at 39% in the last quarter of 2023, 12 months after the peak of headline inflation in Australia, the minimum threshold for claiming a capital gains discount.

Even in pre-pandemic inflation times, when Australia had low inflation, around 26% of investor property capital gains would have had a lower taxable gain under indexation.

Like all things in the Australian property, the market of the investment property matters, as does the time held and the real returns of the asset.

If an investment property was sold in Sydney between 2016-2022 then the capital gain discount would have been significantly more favourable towards the 50% discount. Though in recent times that has become a lot less likely.

First published 12 May 2026

Comments